Most Americans keep their wealth in stocks and bonds. By not holding any bitcoin or other hard assets, they’re betting that inflation won’t erode their savings.

If you’re a Bitcoiner and know someone like this, don’t push bitcoin harder. Show them how it can complement what they already believe in.

That’s the case the article below makes: stocks aren’t a silver bullet, and even a small allocation to hard assets can go a long way.

Stocks fail when you need them most

If you’re under 40, your savings are likely sitting in index funds, tech stocks, or some mix of the two. To grow wealth over your career, that’s a reasonable place to start.

But stocks are not a silver bullet. Owning nothing but stocks leaves you exposed to the risk of a lost decade: 10+ years where your savings end up buying no more than they did at the start. It has happened before, and in today’s environment, the setup could be forming again.

If you started investing after 2009, you’ve watched stocks only go up. The S&P 500 has returned about 15% a year since then. Only two years (2018 and 2022) were negative, but both recovered within 16 months.

That’s not normal. It’s the best sustained run in modern history, and it has trained an entire generation to believe that stocks always recover quickly, that every dip is a buying opportunity, and that time in the market fixes everything.

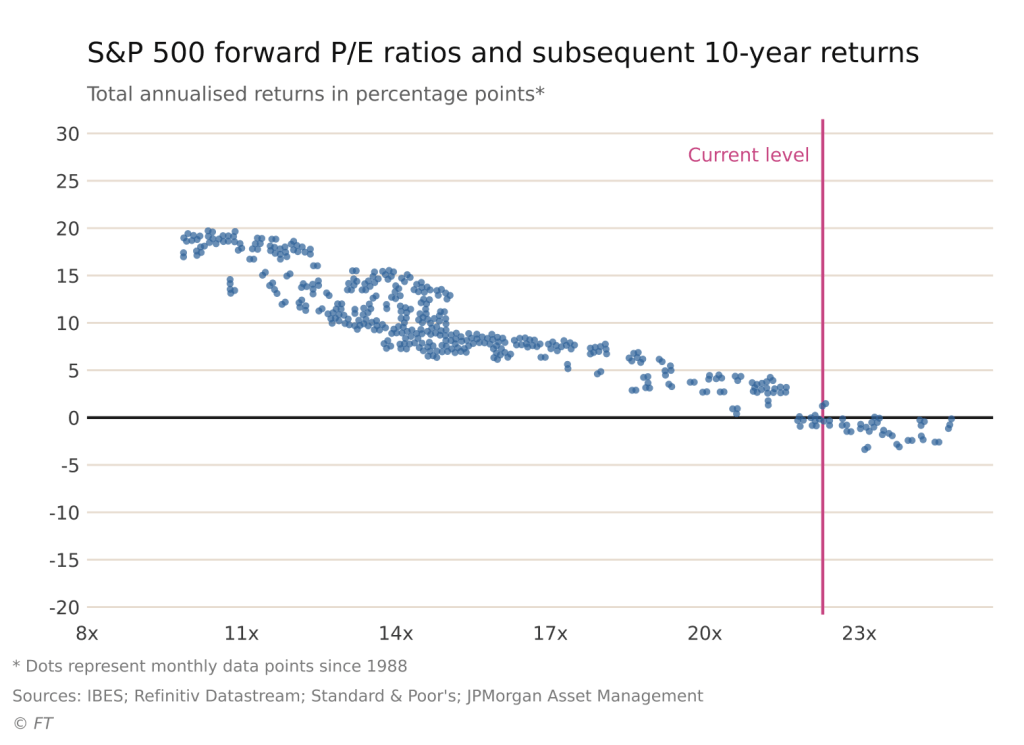

There’s a simple way to judge whether stocks are cheap or expensive: compare their price to the profits the companies are expected to earn. This is known as the forward price-to-earnings ratio, and it currently sits at 22.5, among the highest in decades.

The chart below shows how valuation has historically shaped stock market returns over the following decade. Each dot is a moment in the past, showing how expensive stocks were and what the stock market went on to return over the following ten years.

If history is any indication, stocks this expensive have usually delivered low or negative returns over the following decade. If you do not hold other assets, you risk spending the next decade of your life accumulating no real wealth.

And even if stocks do go up over the next decade, they still have to outperform inflation for you to build real wealth.

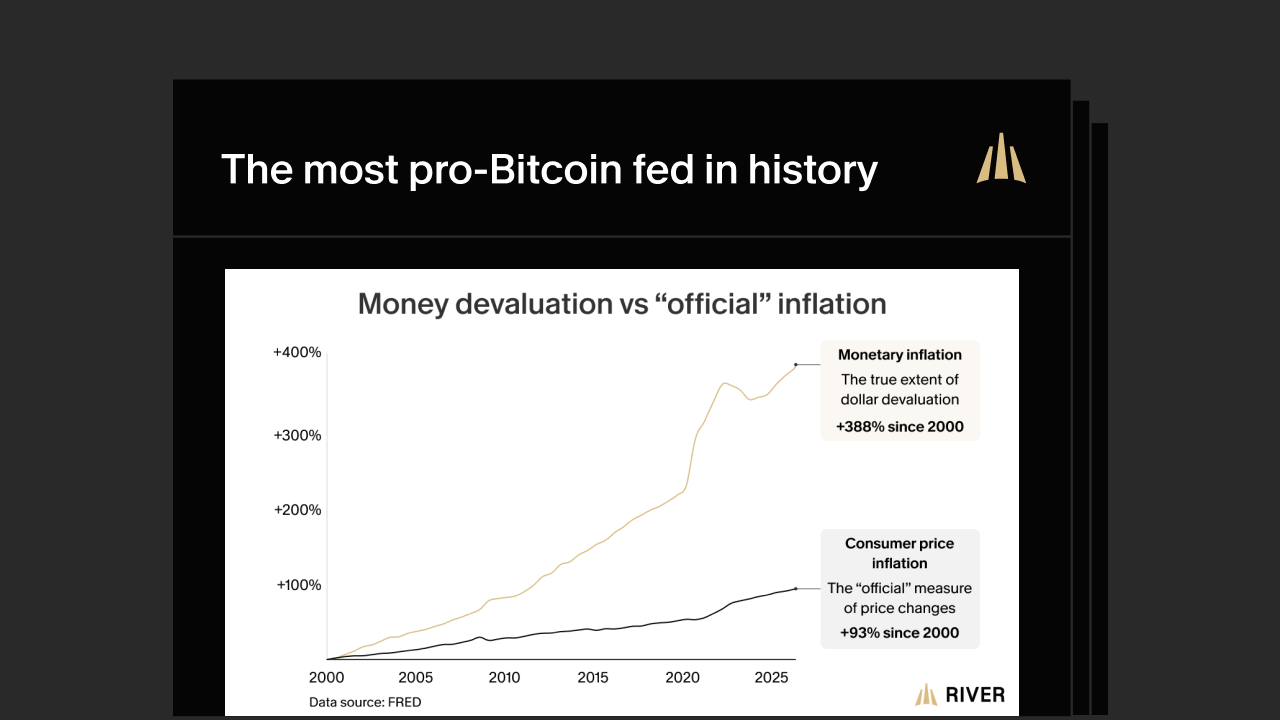

The real villain is inflation

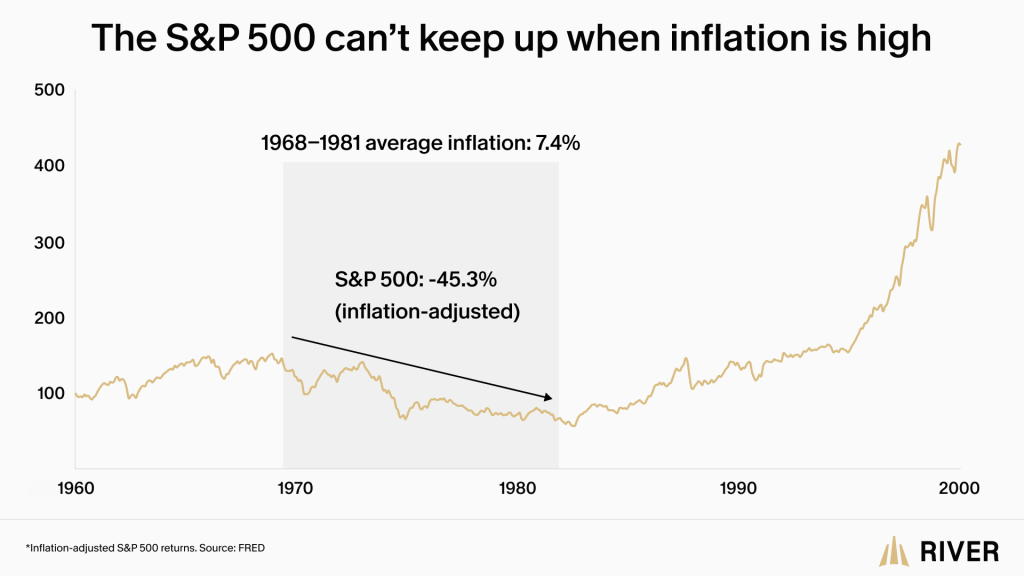

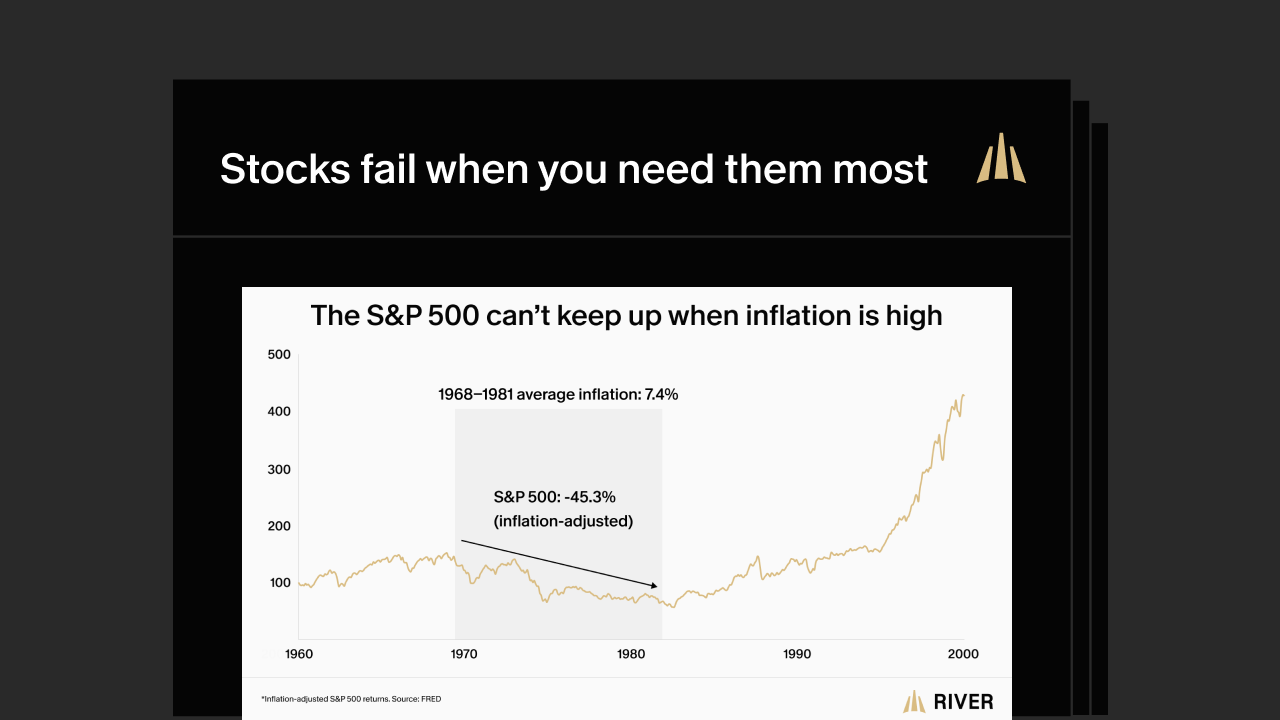

This time could be different. The current wave of AI innovation represents a real opportunity for the economy and stock market. But even the AI boom may not be enough to overcome a decade of high inflation.

In the 1970s, inflation averaged 7%+ a year. After adjusting for inflation, the U.S. stock market lost nearly half its value over 13 years. In comparison, gold rose 5X over the same period.

Applying the same time frame to today, most people cannot imagine seeing their life savings get cut in half by 2039, but history has shown that it is possible.

Inflation is notoriously hard to predict. But here’s what we do know:

- The U.S. government has a debt load of nearly $40 trillion

- The U.S. government is paying $1.4 trillion in interest on this debt each year

- The easiest way for the government to reduce its debt burden is through inflation

There is no alternative. Cutting spending enough to matter means taking away programs people count on, and no politician in either party gets elected on that promise. Inflation is the one way out that requires no vote and no campaign, which is why governments lean on it again and again.

How to protect yourself

Most people have a portion of their savings in bonds, which are historically seen as a safer, more stable investment. But stocks and bonds are exposed to the same underlying risk. When the money loses value, stocks struggle and bonds bleed at the same time.

Neither one is built to protect you from a falling dollar, because neither one is scarce. Companies can always issue more shares. Governments can always issue more debt and more dollars.

What protects purchasing power is an asset whose supply cannot be inflated away.

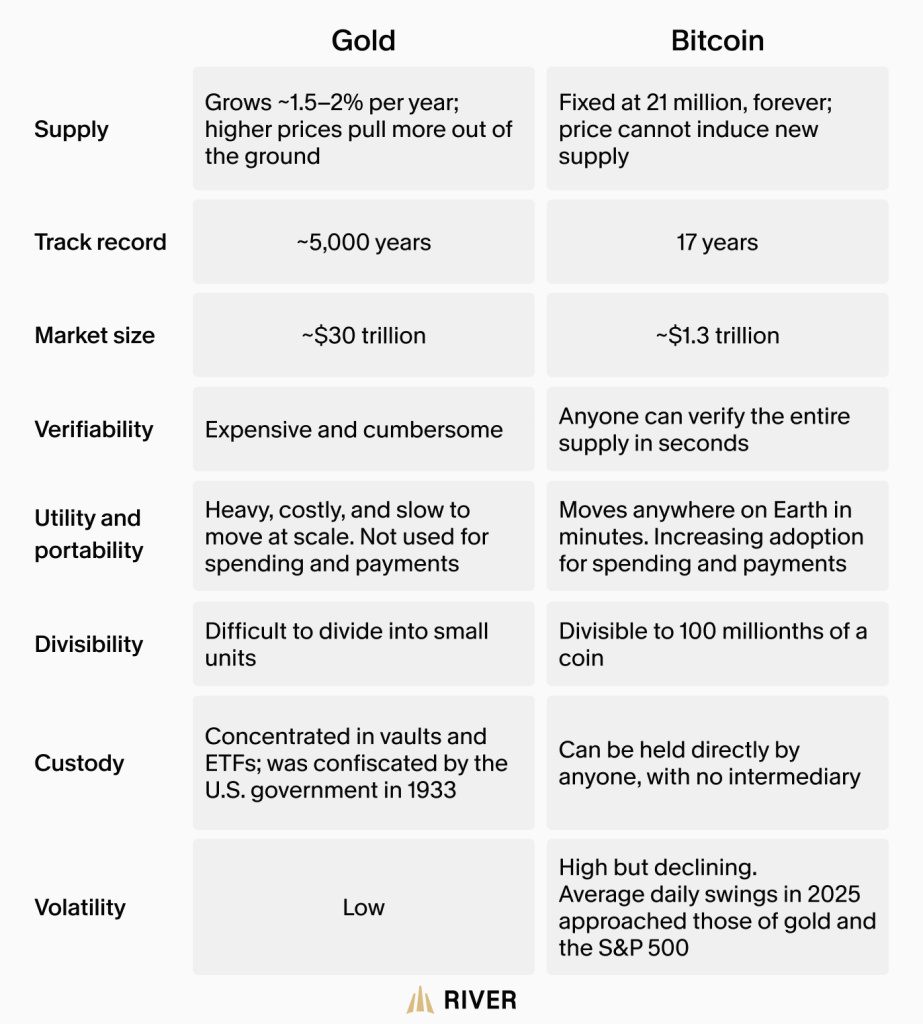

For most of history, that asset was gold. Today, bitcoin does the same job, but in a better way.

Gold’s scarcity is soft: when the price rises, miners produce more, and the above-ground supply still grows by around 1.5% to 2% every year.

Bitcoin’s scarcity is absolute. Its supply is mathematically fixed at 21 million coins, forever, and no amount of demand will change that.

While gold takes days to move and a vault to store, bitcoin settles anywhere on Earth in minutes. Anyone can verify the entire supply in seconds and hold it directly without a bank or middleman that could seize it the way the U.S. government seized private gold holdings in 1933.

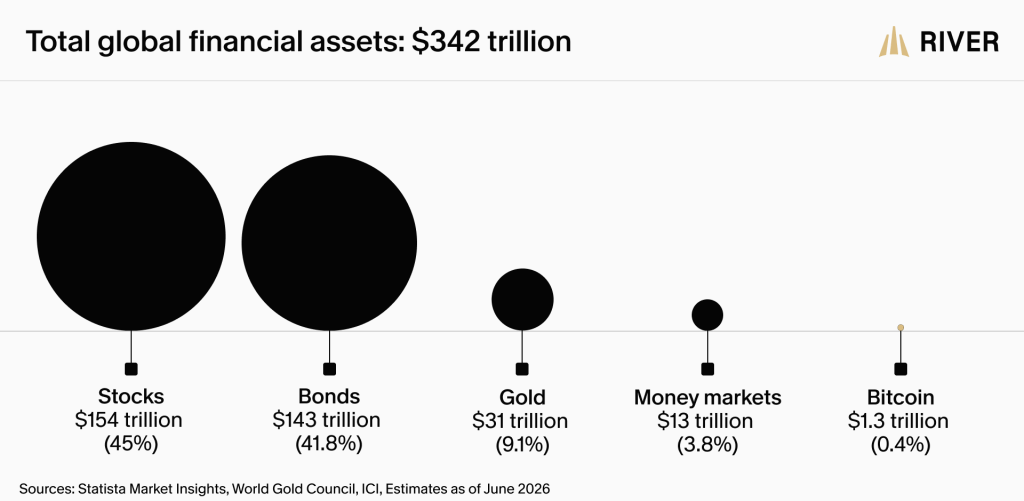

Bitcoin is still small and is worth less than 5% of all the gold ever mined, giving it plenty of room to grow.

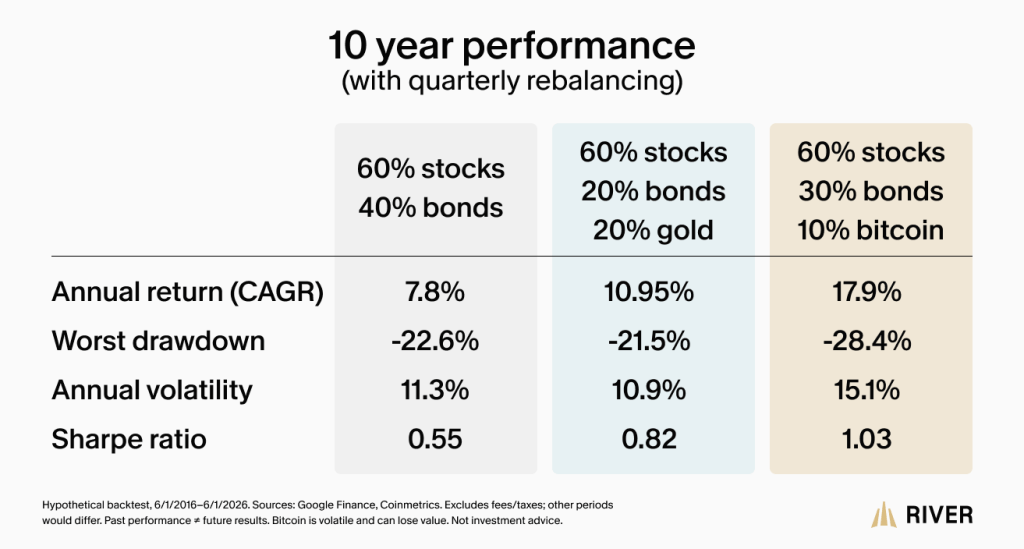

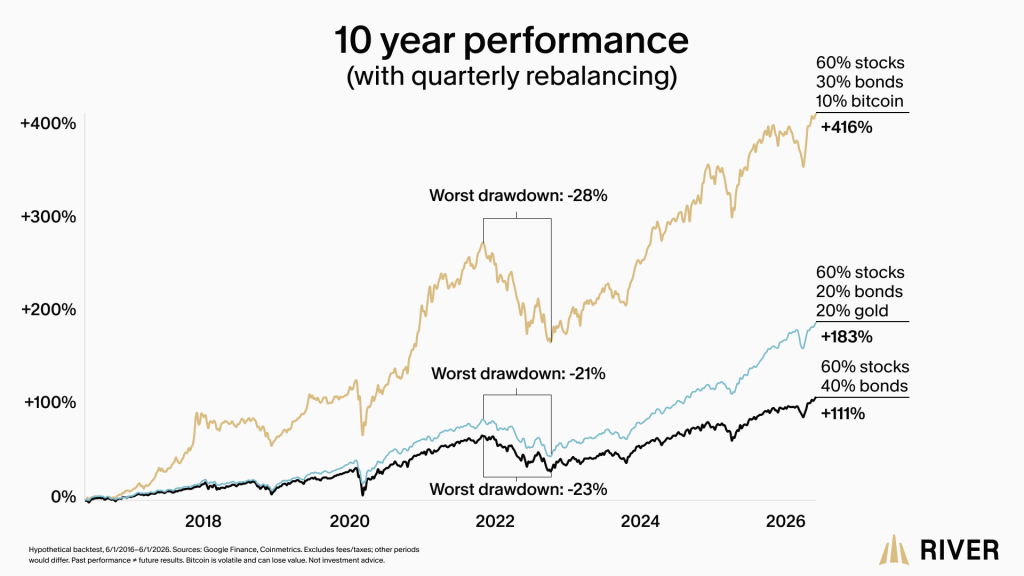

You don’t have to sell all your stocks to protect yourself from bad decades. A small allocation to bitcoin, gold, or both goes a long way.

Over the past decade:

- Putting 10% of your portfolio into bitcoin (from the bond portion of a 60/40 portfolio), would have increased your returns by nearly 4X, while adding only a small amount of volatility.

- Putting 20% of your portfolio into gold would have both increased your returns by ~50% and lowered overall volatility.

Stocks are a good way to build wealth. Hard assets are how you protect that wealth, diversify your exposure, and help secure your financial future.

You don’t have to go all in on hard assets to reap the benefits. Start with a small investment and consider increasing it as your knowledge grows.

This content is for general educational purposes only. It is not investment, financial, tax, or legal advice, and not a recommendation, solicitation, or offer to buy or sell any asset. Bitcoin is highly volatile and speculative; its value can fall rapidly and you could lose some or all of your money. Bitcoin is not FDIC- or SIPC-insured. Any figures shown are historical and/or hypothetical, were measured over a specific past period, do not reflect fees or taxes, and do not predict future results. Statements about future markets, inflation, or returns are opinions, not guarantees. Consider your own circumstances and consult a licensed professional before investing.

You must be logged in to post a comment.